Getting out of debt in New Zealand starts with creating a comprehensive budget to identify surplus income. Next, choose a repayment strategy like the debt snowball or avalanche method. If struggling, contact creditors for hardship assistance under the CCCFA, consider debt consolidation, or seek advice from free services like MoneyTalks before exploring insolvency options.

Debt can feel like an insurmountable mountain, especially with the rising cost of living affecting households from Auckland to Invercargill. Whether it is lingering credit card balances, Buy Now Pay Later schemes, or personal loans, the path to financial freedom requires a strategic approach tailored to the New Zealand banking environment. This guide provides a comprehensive roadmap to regaining control of your finances.

Step 1: Assessing Your Financial Reality

Before you can effectively tackle your debt, you must have a crystal-clear picture of your financial standing. In New Zealand, where the cost of living varies significantly between regions, understanding your disposable income is critical. Ignoring the numbers will only compound the stress.

Calculate Your Net Position

Start by listing every single debt you owe. Do not estimate; log into your internet banking or check your credit report (available for free from Centrix, ilion, or Equifax) to get exact figures. Create a spreadsheet with the following columns:

- Creditor Name: (e.g., ANZ, Westpac, Afterpay, Gem Visa)

- Total Balance Owning: The full payoff amount.

- Interest Rate: This is crucial for choosing your strategy.

- Minimum Monthly Payment: The amount required to avoid penalties.

The Budget Audit

You cannot pay down debt if your outgoing expenses exceed your income. Use a budgeting tool like the one provided by Sorted.org.nz to track your weekly expenses. Differentiate between fixed costs (rent/mortgage, power, broadband) and variable costs (groceries, entertainment). In the current NZ economic climate, reviewing your grocery spend and utility providers (using sites like Powerswitch) can free up vital cash flow to redirect toward debt repayment.

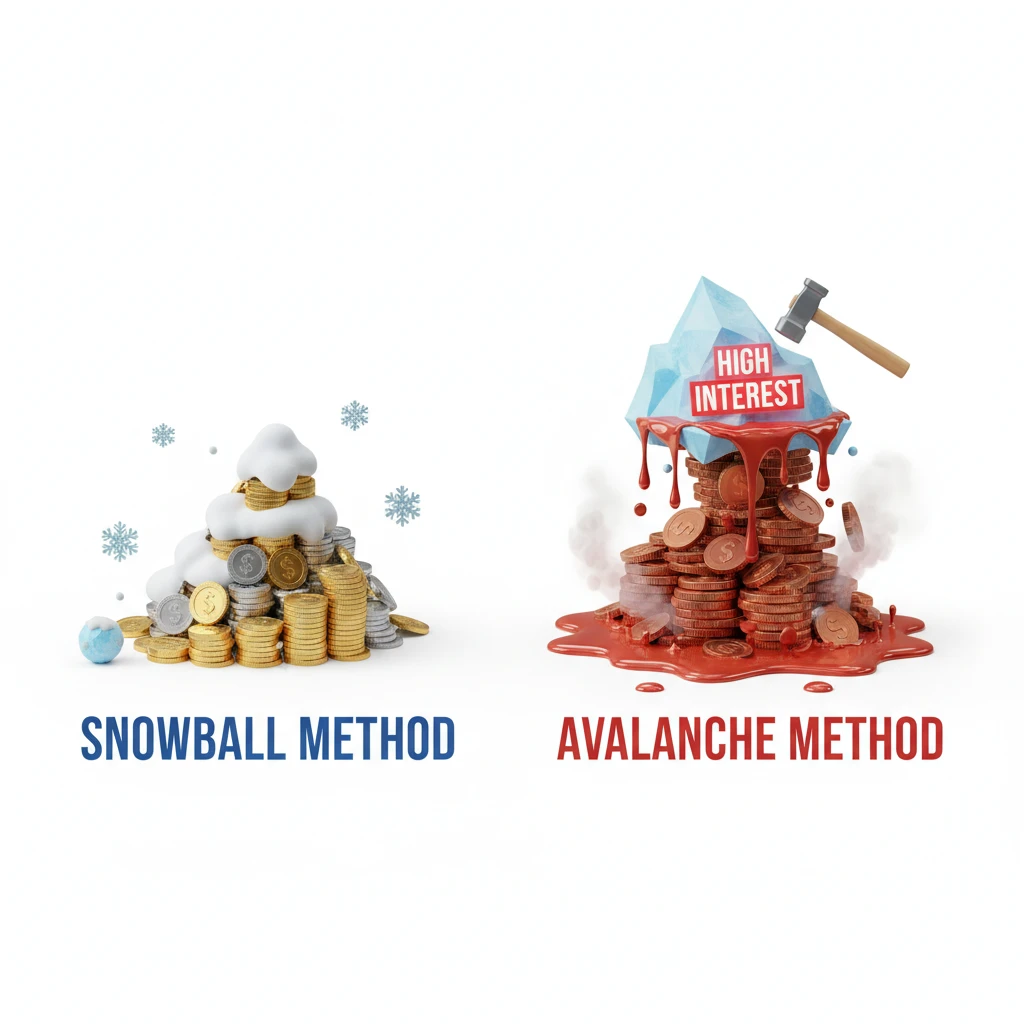

Step 2: Proven Repayment Strategies

Once you have identified a surplus in your budget—even if it is only $50 a week—you need a systematic method to apply it. The two most effective strategies used globally, which apply perfectly to the NZ context, are the Snowball and the Avalanche methods.

What is the Debt Snowball Method?

The Debt Snowball method focuses on behavioral psychology rather than pure mathematics. The goal is to build momentum through quick wins.

How it works:

- List your debts from the smallest balance to the largest balance, regardless of interest rates.

- Pay the minimum repayment on all debts except the smallest one.

- Throw every spare dollar at the smallest debt until it is gone.

- Take the amount you were paying on that small debt and add it to the minimum payment of the next smallest debt.

Why it works: Clearing a Buy Now Pay Later debt of $200 gives you a psychological boost. This motivation is often what keeps Kiwis on track during a long debt-reduction journey.

What is the Debt Avalanche Method?

If you are mathematically inclined and want to save the most money possible, the Avalanche method is superior.

How it works:

- List your debts from the highest interest rate to the lowest interest rate.

- Pay minimums on everything else.

- Focus all extra payments on the debt with the highest interest rate (often store cards or payday loans which can exceed 20% p.a.).

Why it works: By attacking the most expensive money first, you reduce the total amount of interest paid over the life of the loans, getting you out of debt faster mathematically.

Step 3: Debt Consolidation in NZ

Debt consolidation involves taking out a single new loan to pay off multiple smaller debts. This simplifies your finances into one repayment, ideally at a lower interest rate.

Balance Transfer Credit Cards

Many New Zealand banks (such as Westpac, BNZ, and ANZ) offer balance transfer rates, sometimes as low as 0% or 1.99% for a fixed period (usually 6 to 12 months). This can be a powerful tool if used correctly.

The Trap: If you transfer your balance but continue to spend on the old card, or fail to pay off the debt before the low-interest period ends, you may end up in a worse position. The standard interest rate will apply to any remaining balance after the promotional period.

Debt Consolidation Loans

Personal loans for debt consolidation are available through banks, credit unions, and peer-to-peer lenders like Harmoney or Lending Crowd. The interest rate you are offered will depend heavily on your credit score. Be wary of “second tier” lenders who may charge high fees and interest rates comparable to the debts you are trying to clear.

Key Advice: Only consolidate if the new interest rate is significantly lower than the weighted average of your current debts, and ensure you close the old accounts immediately.

Step 4: Negotiating with Creditors & Hardship

If budgeting and strategy aren’t enough because you simply cannot meet your minimum obligations, you need to communicate with your creditors immediately. In New Zealand, you have legal protections under the Credit Contracts and Consumer Finance Act (CCCFA).

Unforeseen Hardship Applications

If you have experienced a change in circumstances—such as illness, injury, loss of employment, or the end of a relationship—you can apply for a hardship variation.

What to do:

- Contact your bank or lender’s “Financial Hardship” team.

- Submit a written application explaining your situation.

- Request a “payment holiday” (deferral) or an extension of the loan term to reduce weekly payments.

Important Note: While a payment holiday gives you breathing room, interest usually continues to accrue, meaning you will owe more in the long run. It is a temporary fix, not a permanent solution.

Free Financial Mentoring

You do not have to do this alone. New Zealand has a network of free financial mentors. MoneyTalks (0800 345 123) is a free helpline available to all New Zealanders. They can connect you with a local budget service that can advocate on your behalf, often achieving better negotiation results with creditors than you might achieve alone.

Step 5: Insolvency and Bankruptcy in NZ

When repayment is mathematically impossible, New Zealand’s Insolvency and Trustee Service (ITS) offers formal legal procedures to manage unmanageable debt. These should be considered last resorts as they have significant long-term impacts on your credit rating and ability to borrow.

No Asset Procedure (NAP)

The NAP is unique to New Zealand and is designed for those with “no realizable assets” and lower debt levels.

- Criteria: You must owe between $1,000 and $47,000. You must have no means of repaying the debt and no assets (excluding essential household items and a vehicle worth less than $6,500).

- Outcome: Your debts are cleared after 12 months.

- Impact: It remains on your credit file for four years. You cannot borrow more than $1,000 without disclosing your NAP status.

Debt Repayment Order (DRO)

Formerly known as a Summary Instalment Order, a DRO is a formal agreement where you pay back a portion of your debt over time under the supervision of a supervisor.

- Criteria: Unsecured debt under $50,000.

- Mechanism: You pay what you can afford for 3 to 5 years. Creditors cannot chase you during this time.

Bankruptcy

This is the most severe option. If you owe more than $47,000 (or less, but have assets), you may file for bankruptcy.

- Consequences: The Official Assignee controls your assets and finances for three years. You may need to contribute part of your wages to debts. You cannot be a company director or travel overseas without permission.

- Duration: Bankruptcy usually lasts for three years, but the record stays on the insolvencies register permanently and your credit file for seven years.

Step 6: Utilizing KiwiSaver for Hardship

Many Kiwis look at their KiwiSaver balance as a potential lifeline. While KiwiSaver is designed for retirement, there are provisions for Significant Financial Hardship withdrawal.

You may be able to withdraw your contributions (and your employer’s) but not the Government contributions if you cannot meet minimum living expenses. This includes inability to pay for:

- Minimum food and grocery needs.

- Accommodation (rent or mortgage interest).

- Medical treatment.

The Process: You must apply through your KiwiSaver provider, not the IRD. You will need to provide exhaustive evidence of your budget and debts. It is highly recommended to speak with a budget adviser before applying, as providers often require a sign-off from a financial mentor to prove you have exhausted other options.

Frequently Asked Questions

Does debt consolidation hurt my credit score in NZ?

Initially, applying for a consolidation loan may cause a small, temporary dip in your credit score due to the credit inquiry. However, if you use the loan to pay off high-interest debts and make regular, on-time payments on the new loan, your credit score will generally improve over time as your credit utilization ratio decreases.

Can I go to jail for debt in New Zealand?

No, you cannot go to prison simply for owing money to banks or lenders in New Zealand. However, ignoring court orders or committing fraud (such as lying on a loan application) can lead to legal consequences. It is vital to engage with the legal process if you receive court documents.

What is the statute of limitations on debt in NZ?

Generally, the limitation period for debt recovery in New Zealand is six years under the Limitation Act 2010. If you have not made a payment or acknowledged the debt in writing for six years, the creditor may be statute-barred from enforcing the debt through the courts. This does not apply to all types of debt, such as taxes or child support.

How does the No Asset Procedure affect my future borrowing?

The No Asset Procedure (NAP) remains on your credit record for four years. During this time, and potentially for years afterward, you will find it extremely difficult to obtain credit, a mortgage, or even some utility contracts. Lenders view a NAP as a significant risk factor.

Should I use a debt collection agency or settle directly?

It is almost always better to negotiate directly with your original creditor before the debt is sold to a collection agency. Once a debt is with a collector (like Baycorp), they are focused on recovery. However, you can still negotiate payment plans with agencies. Never agree to a payment plan you cannot afford.

Is money in my KiwiSaver safe from creditors?

Generally, yes. Creditors cannot touch your KiwiSaver balance to recover debts, even in bankruptcy, provided the funds remain in the scheme. The Official Assignee cannot usually access these funds. However, once you withdraw the money, it becomes an asset that can be claimed.