Best Ways to Manage Your KiwiSaver Monies

Advice on optimizing KiwiSaver contributions, fund selection, and withdrawal strategies for New Zealanders.

Hey New Zealanders! Ever wondered how to get the most out of your KiwiSaver? You’re in the right place! We’re diving deep into the best ways to manage KiwiSaver monies so you can make smart choices for your future. KiwiSaver isn’t just a savings scheme; it’s a powerful tool for your financial well-being, whether you’re saving for your first home or getting ready for retirement. Knowing the ins and outs can seriously boost your savings, so let’s unlock its full potential together. Get ready to level up your financial game!

Understanding KiwiSaver Contributions

When it comes to the best ways to manage KiwiSaver monies, understanding how contributions work is ground zero. It’s like knowing the rules of a game before you start playing! Your KiwiSaver balance grows from a few different places, and getting these right can make a huge difference.

Employee Contributions: Your Input

If you’re working, you get to choose how much you contribute from your pay. The standard options are 3%, 4%, 6%, 8%, or 10% of your gross (before tax) salary. The money comes straight out of your pay, so you don’t even have to think about it! It’s super easy and a fantastic way to consistently save. The more you put in, the more your KiwiSaver monies grow over time. Even a small increase can add up big!

Employer Contributions: Free Monies!

This is where it gets good! If you’re contributing at least 3% of your gross pay, your employer generally has to contribute at least 3% of your gross pay too. This is literally free money for your future, on top of your wages! Make sure you’re getting this, because it’s one of the absolute best ways to manage KiwiSaver monies by getting extra cash without doing anything extra.

Government Contributions: The Annual Boost

The government wants you to save too, so they give you a little bonus each year. For every $1 you contribute (up to $1042.86 per year), the government will put in 50 cents, up to a maximum of $521.43. To get the full $521.43, you need to contribute at least $1042.86 yourself between 1 July and 30 June each year. If you’re not hitting this target, you’re leaving free money on the table! This yearly boost is a key part of the best ways to manage KiwiSaver monies effectively.

Voluntary Contributions: Supercharge Your Savings

Want to go above and beyond? You can make extra contributions directly to your KiwiSaver provider anytime you like. This is awesome if you have some spare cash and want to give your savings an extra kick. Think of it as hitting the nitro button on your financial future! Using these voluntary contributions wisely is another one of the best ways to manage KiwiSaver monies, especially if you have specific goals in mind.

Here’s a quick look at how different contributions can stack up:

| Contribution Type | How it Works | Benefit |

|---|---|---|

| Employee | 3%, 4%, 6%, 8%, or 10% from pay | Consistent savings, direct from wages. |

| Employer | Minimum 3% (if you contribute). | Free money, boosts your total balance. |

| Government | 50 cents for every $1 you contribute (up to $521.43). | Annual top-up for meeting target. |

| Voluntary | Direct payments to your provider. | Accelerate savings, reach goals faster. |

Choosing the Right KiwiSaver Fund

So, you’re contributing regularly, awesome! But just putting money in isn’t the only thing. One of the truly best ways to manage KiwiSaver monies is making sure your money is invested in the right type of fund. Think of it like choosing the right vehicle for a road trip – a sports car for speed or a sturdy SUV for rough terrain.

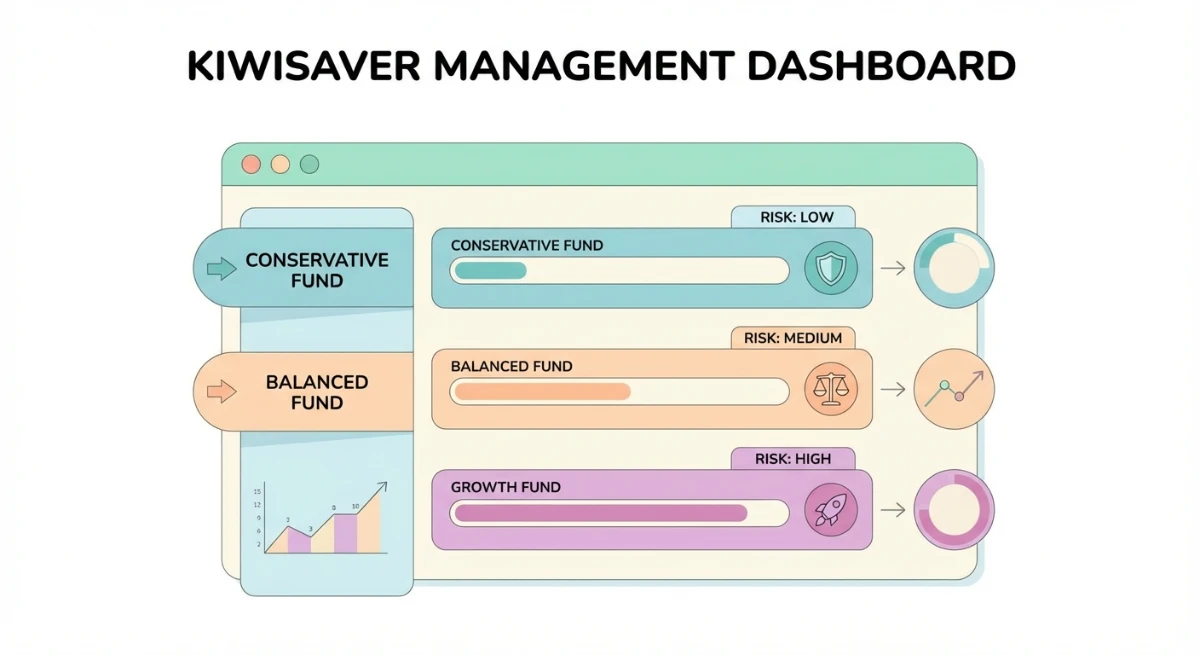

Understanding Fund Types: Risk vs. Reward

KiwiSaver funds generally fall into a few categories:

- Conservative Funds: These are for the super cautious. They invest mostly in lower-risk stuff like cash and bonds. You won’t see huge gains, but you also won’t see huge drops. Good if you’re close to withdrawing your money.

- Balanced Funds: A mix of conservative and growth investments. They aim for steady growth with moderate risk. A good middle-ground for many people.

- Growth Funds: These are for the adventurers! They invest more in shares and property, which can go up and down a lot. Higher risk, but potentially higher returns over the long run. Best if you’re young and have a long time until retirement.

- Aggressive Funds: Even more shares, even more risk! These are for those who are comfortable with big swings and have a long time horizon.

What Fund is Right for YOU?

This is super important for the best ways to manage KiwiSaver monies. Your age and how long you plan to keep your money in KiwiSaver (your